This is not a secret any longer: China’s costs have been relentlessly on the rise for the past decade while South East Asia and India have been aggressively taking more shares in the sourcing landscape.

Although the recent US-China tariff war has attracted most of the public attention, it is clearly not the deep cause of the restructuring the Chinese textile, apparel and bags industry is experiencing.

The industry is undergoing a genuine and critical evolution that shifts China’s position in the industry within Asia and could be challenging its significance as a competitive supplier for textiles and textile byproducts.

To give more insight into this changing landscape, we will be exploring the current status of China, from a sourcing perspective

At this stage what are the strengths and weaknesses of the apparel & bags industry in China

What is the impact of the changing business conditions on the industry

How Chinese apparel and bags manufacturers are still developing

WHAT HAS CHANGED ?

Understand how the Chinese sewing industry business conditions are not as favorable as they used to

Relatively high costs are one of the main weaknesses of the industry

Relentlessly rising wages and land cost burden the competitiveness of Chinese businesses

The cost of work has more than doubled in 10 yrs

Labor costs can now account up to 50% of the FOB price of a product in products of labor-intensive industries such as the sewing industry

China housing price change y.o.y (monthly measurement) in %. Source : National bureau of Statistics China

The cost of means of production surged

Inflation in land and property prices in particular has been ramping. In 2018 only, housing prices rose by 8.6% compared to previous year. This is covers both personal housing and industrial property.

Ask anyone in China : it is difficult to find workers in the sewing industry

What has made this group of population scarcer?

Source : National Bureau of statistics

China is undergoing a “Back to hometown” population move.

Of all regions of China, only the coastal areas are emptying while all other provinces in China welcome more people year on year.

Traditional manufacturing areas of China (Eastern coast) are not attracting new workers any longer.

More workers choose to be back in their province of origin close to their family and find work there.

The depletion of available skilled workforce in these traditional manufacturing areas is one of the factors leading to a perceived lack of workers.

Source : national Bureau of Statistics China

China population is getting more and more educated

Over the years, more and more young people are getting university degrees and do not intend to become simple workers.

With more than 8 million students entering the University in 2019, this trend is not soon to be inverted. (national bureau of Statistics China) .

Despite China’s very large population, it becomes more and more difficult to hire qualified personnel as workers in labor intense industries such as the Textile industry,

This is particularly striking in the sewing industry, where staff under 40 are now hardly seen.

The shrinkage of the pool of available workforce in the long term affects the manufacturing industry in the country as a whole.

The Central government sets the tone

Evict labor intense industries out of the “hot zones” and scale up the country’s products offer instead

As a countrywide development strategy, the Central government has a clear and strong policy to move labor intensive industries further west of the country or out of China and leave space for the tertiary industry or high tech businesses.

Under the "Made in China 2025" plan, Chinese authorities assert their determination to shift economic development driven by manufacturing to one that is steered by innovation.

This plan followed by China’s 13th five-year plan (2016-2020) confirms that China does not intend to grow as an exporter for apparel and bags.

See below brief comments on China 13th five-year plan for textile and apparel, which is far from ambitious.

Practically, this Central direction translates into strong measures being implemented to reach the fixed goals. Among them are the cancelling of subsidies for T&A industries in the coastal areas, additional subsidies to tech intensive industries (such as IT) and the strengthening of government checks (environmental, tax and insurance compliance) on labor intense businesses and related industries (such as trims manufacturers).

In this context, low-cost mass production industries in Guangdong are rapidly leaving space to tertiary and high-tech industries.

SE Asian countries sewing industry gained muscle

SE Asia can potentially receive the orders that were once intended to China. This is especially true since the 2018 US tariffs war

As Chinese businesses are struggling to keep their costs to a level that complies with customers price expectations while still generating margins, most of SE Asian countries still benefit from low cost labor and reasonable production costs.

In addition, some countries like Vietnam, being China neighbors, benefit from this geographical proximity to traditional hubs in China : manufacturers there are able to reduce costs with limited interruption or delays in their existing supply chains

For this reason, large volume, low price orders have already partially moved out of China and are now being made in SE Asia or in India.

The tariff war that started in 2018 has only accelerated this shift making it even more difficult for China businesses to match expected prices. Some brands have even required their Chinese manufacturers to set up new lines in SE Asia as a condition to keep on working with them.

What has changed

for the apparel and bags

industry in China :

· Higher costs

· Scarcer labor force

· “labor intense industry removal” government strategy

· Strengthening of neighboring competitors

HOW BIG IS THE IMPACT OF THOSE CHANGES?

Did China’s competitiveness and market shares

show a drop recently and to what extent?

Does the “world factory”remain in Pole position?

The status of China market shares

While China unshakably remains the world’s largest apparel exporter, China’s market shares in the world’s top three largest apparel import markets (namely the United States, EU, and Japan) show a clear declining trend over the past five years.

Source : U.S. Department of Commerce, Office of Textiles and Apparel (2018) / Eurostats

If we investigate bags and luggage business, China did give up US market shares in favor of Vietnam and Philippines mainly, while its business volume with Europe seems to be more stable.

This can be explained as large quantity / low-price orders (mainly intended to the US market) are not workable in China any longer, cost wise.

Productions intended for Europe, on the other hand, probably include more of the small to medium quantity / reasonably priced orders that are still suitable to be made in China.

These statistics will have to be updated as 2019 statistics of China exports will probably show drops as businesses shifted production away from China in the second half of 2018.

How price competitive is China now?

How Chinese manufacturers prices reflected the rise in their costs?

Despite reported cost increases and societal changes that do impact costs (as described in Section 1), 2017-2018 figures show that prices of apparel imports from China have gained competitiveness in comparison to their competitors.

in 2018, Chinese import prices are 27% cheaper than those of Vietnam and 14% than those of Bangladesh.

Indeed, despite unfavorable cost trends, Chinese manufacturers still benefit from indisputable cost advantages such as :

Proximity to low priced fabrics and trims

Competitive and efficient transportation and export facilities

Productivity and management efficiency

Quality compliance of products

Declining Chinese currency vs USD

Increased export-tax rebates

Although the above figures shall be updated for 2018-2019, it must be said that thanks to the above factors, the pain for exporters arising from US tariffs should be limited.

The impact of

tougher conditions

on China T&A business :

· Clear drop of business volume with the US

· relatively stable business volume with EU

· Increased price competitiveness compared to competitors

HOW DO CHINESE APPAREL AND BAGS MAKERS BYPASS DIFFICULTIES?

The previous sections can feel contradictory :

- On one side, China’s inner factors show a deteriorating business environment for apparel and bags manufacturers

- On the other side, results up to mid-2018 show a low (or even contrary) impact on prices and business volume

The relatively good results of the Chinese T&A industry up to last year is certainly due to its extraordinary agility.

Indeed, while some manufacturing units simply bankrupted, others adapted.

The responses of the Chinese apparel industry to the changes within and outside China have been multiple and can explain why China exports remain almost stable in 2017-2018 and how prices got even more competitive.

How are CHINESE BUSINESSES adapting to the new game rules?

What is to be expected from Chinese textile, apparel and bags businesses in the near future?

a/Move to Northern or Western China

Lower labor costs and government incentives push entrepreneurs West

China’s T&A manufacturing base is gradually moving from the east coast to the western and central part of the country.

These regions are accounting for 22.5 percent of China’s T&A production in 2014 (up from 16.8 percent in 2010), this share may further increase to 28 percent by 2020.

We have indeed seen in the past year, countless sewing units being entirely or partially moved to remote areas.

Smaller businesses may have entirely moved to the western or norther regions, keeping at most a liaison office in Guangdong while larger manufacturers have chosen to multiply their production sites.

For example, many of the formerly 1000 and above workers sewing units on the east coast have shrunk to a few hundred employees while new branches of the same companies were opened in the central and western parts of the country, welcoming hundreds of workers.

To apparel and bags manufacturers, the attractivity of remote areas of China mainly lies in :

· a local workforce at lower cost

· government incentives for new investments in labor intensive industries.

1- Lower labor costs

In the apparel and bags industry, labor cost accounts for 35% to 55% of the total cost of a product. From this ratio, we easily understand that cutting on labor costs is a certain way to gain competitiveness and/or grow margins.

Although the urban–rural income gap in China has started to decline since 2007, urban income is still 2.7 times higher than the one of rural households in 2017.

In addition, while factories on the Chinese eastern coast usually have to provide meals and accommodation for free on top of wages, factories in remote areas hire more of the local workforce who return home at night and sometimes do not require the employer to arrange and pay for meals.

While we can expect that the cost of labor in remote areas will in fine rise, the trend is still that urban income grows faster than rural income, which may induce that relocation is making economic sense in the medium run : the current countryside labor force is a solution to rocketing wages in the traditional manufacturing areas.

2- Local government incentives

As a bonus, and to attract investors, several rural counties subsidize the openings of new factories (granting tax benefits, power subsidies, providing buildings and land for free as well as helping in recruiting workers) : this is an additional competitive advantage to these relocated manufacturing units as they not only benefit from cheaper labor costs but also lower costs of means of production.

Labor intense industries such as sewing factories are light and cheap to move. Considering the potential gains as described above, the cost of change vs competitiveness gain ratio is very high, which makes this choice of moving inwards China one of the preferred alternatives for existing factories.

This competitiveness boost of moving to rural areas can partly explain the surge in competitiveness that is related in the US imports price statistics described in Part 2.

"China moves its factories back to the countryside" Financial times 2019 Limited

b/ Climb up the value chain

Offering higher end products is the natural step ahead for many manufacturers

With several decades’ history of manufacturing textile, garments and accessories as the world factory, China has trained and grown a highly skilled workforce in textile development, sewing and pattern making for bags and apparel.

Although this workforce is ageing it is still available and could well be the major asset to China’s T&A industry: it is what neighboring competitors do not have yet.

With this strong know-how, developing and producing higher end products is the natural step ahead for many manufacturers.

That could explain why the market share of China in the EU is rather stable: Chinese factories can offer more complex products guaranteeing certain quality standards. This type of products is not easily relocated to newer low-cost countries.

In addition, more demanding products are naturally purchased at a higher price. This makes it possible for Chinese factories to stay on this market while standing the rise in wages.

c/ Innovate

Boost efficiency with technology, offer groundbreaking products

T&A companies in China are encouraged to increase spending on research and development (R&D), which on average had accounted for 0.47%of T&A companies’ sales revenue in 2013, up from 0.43% in 2011.

1- Rely on technology to boost productivity

With a grounded experience in production and supply chain management, as well as abundant machine manufacturers, Chinese factories have assets in hand to reflect on their processes and boost their efficiency through increased automation.

According to a 2018 USFIA (US Fashion Industry Association) bench marking study, the adoption of automation technology, improved supply chain efficiency, and currency factors could explain the demonstrated price competitiveness of Chinese apparel.

2- Research and offer differentiative materials

Apparel and bags factories can rely on the dense network of Chinese by-suppliers to offer their customers innovative products using advanced materials.

Whether talking about “smart” fabrics, recycled materials or more simply “fancy finishes” materials, China remains the number one sourcing destination.

For example, China is the major global supplier of recycle-base polyester fiber: it produces over 4 million ton of rPSF (or rPET) which is used in domestic spinning and non wovens and is also exported in fiber form. In addition, China has huge overcapacity in recycled polyester manufacturing, with around only 50% capacity utilization, which can make us think that China will strengthen its position as the world’s biggest supplier of recycled polyester (rPET) in the future. (Source : Textile Beacon’s Global Markets)

This invaluable source of innovations is fed by constant research work while encouraged by public funding (new textile materials development is officially supported in the “Made in China 2025” plan).

Using those cutting-edge materials is a way for Chinese factories to move to more specific (and probably higher end) products which are more suitable to the current business conditions in China.

d/ Turn to the domestic market

The huge and growing China domestic market is just ready at hand

1-Take advantage of the boosting predominant e-market

The rise of China’s online “e-tailers” have transformed the way Chinese people shop: in 2015 nearly half a billion Chinese shopped online spending 589 billion USD in total and this figure is to still increase according to the current forecasts.

The online-shopping phenomenon supported and still encourages the growth of a multi-billion dollar express delivery industry (more than 8000 express companies are now operating) and a plethora of e-commerce related service companies.

Using this strong network, Chinese factories can relatively easily enter this E-market, whether directly with own online shops or indirectly , manufacturing for local buyers selling online.

2- Enter a growing market with more buying power

China’s middle class already outnumbers the entire population of the United States and is expected to reach 600 million by 2020. With such a projected market size, China is expected to become the world’s first global market by 2025.

The average Chinese consumer is under 35 and likely to shop mostly via mobile device; as incomes rise, these consumers are looking for quality products, and they are buying them online.

This means that now is the perfect time for even small companies to start selling to China.

3- Surf on the Patriotic wave with entrusted Chinese brands

Chinese brands have regained the local consumers‘hearts : they have upgraded their quality standards and communicated it to consumers using their better insight of the local market and of the ways to reach it.

As Chinese consumers do not perceive a difference in quality between a foreign brand and a domestic one, they tend to turn more to domestic brands (Chinese consumers are leaving multinational brands on the shelves) : a 2016 report by McKinsey found that 62% of surveyed Chinese consumers would prefer a domestic brand for the same product/quality/price.

This results in local brands gaining strength and shares in China : already 30 of the top 50 Fast Moving Consumer Goods brands are now local, up from 20 five years ago. Six of the top seven mobile-handset brands are also local today (Source : McKinsey “what can we expect in China 2019”).

China’s huge and welcoming market readily reachable at one’s door is of course a tempting opportunity to all Chinese manufacturers : it can compensate the decrease of business volumes coming from abroad and develop further in the long run as the apparel and bags consumption in China is projected as surging in the coming years.

While some apparel and bags manufacturers venture into registering their own brand and start e-retailing, other are tying up with domestic customers who in turn manage sales on the net.

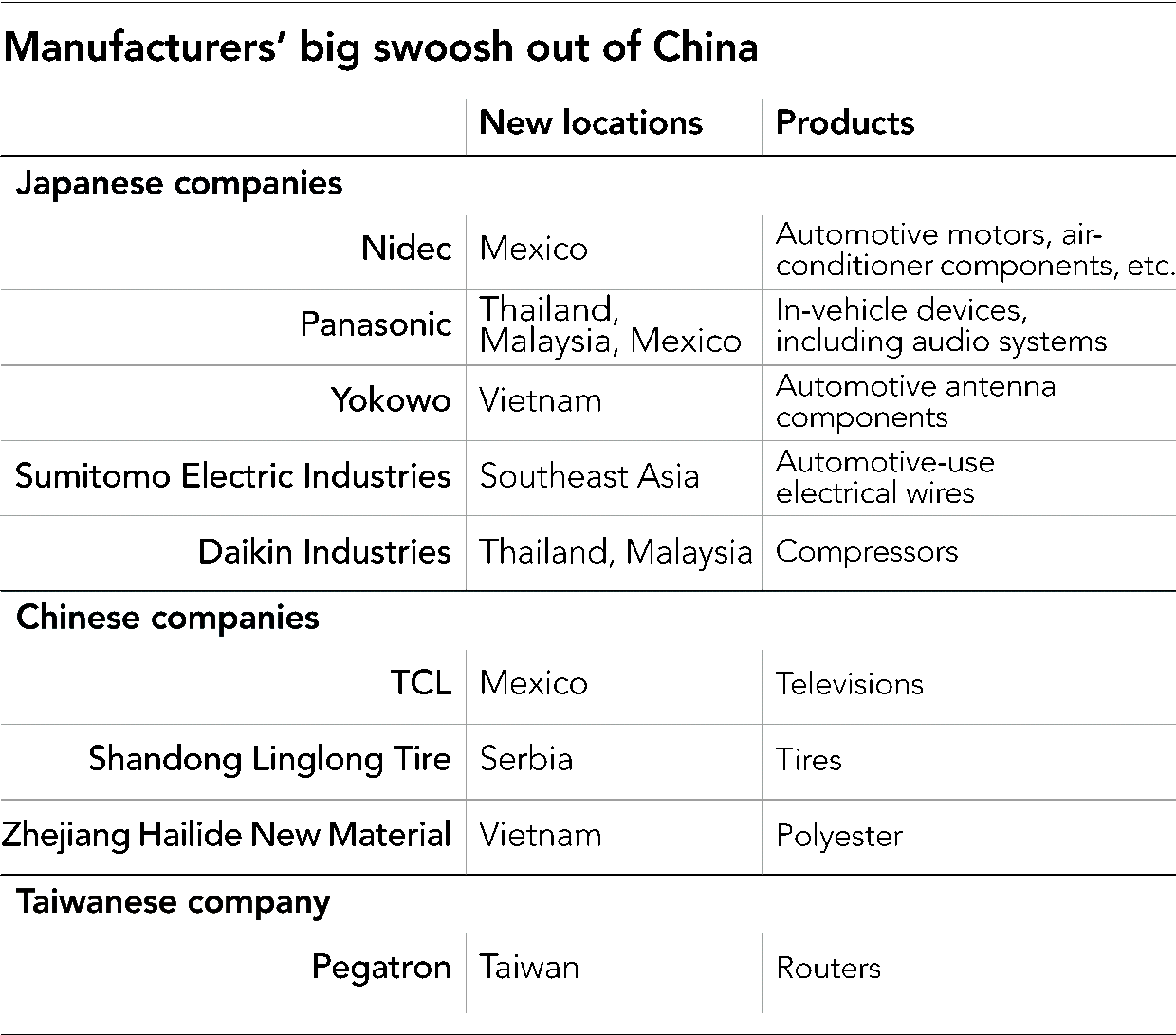

e/ Move or re-mix production configurations out of China

China is investing heavily in neighboring countries to install new facilities

With the US government restricting purchases from China for its own purchases of goods and discouraging its vendors to do so, a broad range of US companies see a risk in buying from Chinese suppliers and require that their products are made elsewhere.

That is how, in order to keep and possibly grow their customers, some factories chose to move their know-how to lower cost countries (Vietnam, Cambodia, African countries) : while keeping a smaller plant in Mainland China, new branches of Chinese manufacturers are opened in south east Asian countries or in Africa for subcontracting or direct manufacturing.

This deployment of production units outside China has already been going one for several years : as the country moves up the value chain, old-school labor like basic stitch-and-sew apparel manufacturing is leaving the country.

The US-China tariff war started in 2018 dramatically accelerated this movement with electronic parts factories being first to move out of China rapidly.

Only in our neighborhood have we seen an electronics plant of 5000 workers emptying and moving to Cambodia within 3 months.

Within our industry, one of the bags manufacturers we work with, which three main customers are American hurriedly made plans to build 3 to 5 sewing lines in Vietnam to keep their business going. The existing China factory will remain, in charge or product development and procurement, the line will be running production processes requiring advanced technology only.

With this transfer, upstream businesses such as fabric mills are also setting up new facilities in these new apparel and bags manufacturing locations : Zhejiang Hailide New Material, a major Chinese polyester producer, will spend $155 million to build its first overseas plant in Vietnam, planning to bring it online by mid-2020.

It can be expected that, through this move, the apparel and bags industry in the neighboring countries (especially within the Asean group) would profit from a definite boost in competitiveness and efficiency, making their competition with remaining China factories fiercer.

Indeed, deploying new manufacturing units abroad is not only about investing money, building factories and installing machines: it is also about transferring production management know-how. Chinese factories usually export their operational teams to the new locations in a view to train up workers and local managers abroad.

In addition, with upstream businesses also deploying outside China, materials and trims will be available in quantity and locally and China will in fine loose its advantage of sourcing materials locally at a competitive price. This will affect price and lead times positively for manufacturing units in SE Asia and India.

CONCLUSION

It is undeniable that the Chinese textile, apparel and bags manufacturing industry is undergoing great changes and they are still developing as I am writing.

Although it is difficult to predict the future of our industry in China, we can have glimpse through to clear directions it has already started to take.

What a buyer could expect from China apparel and bags manufacturers in this new business environment ARE the following:

Innovative and complex products that no other low-cost country is for now able to produce

A relatively high level of service thanks to its acquired know-how and strong pool of upstream suppliers

More flexibility for smaller quantity orders

Less dependence on foreign orders as domestic demand bursts

Possible alternative with these same companies to produce at lower cost in their overseas branches

Plan ahead ! Download the China Holidays calendar for 2023